Home

/ How To Find Long Run Equilibrium Price In Perfect Competition - An increase in the market demand for oats, from d 1 to d 2 in panel a , shifts.

How To Find Long Run Equilibrium Price In Perfect Competition - An increase in the market demand for oats, from d 1 to d 2 in panel a , shifts.

How To Find Long Run Equilibrium Price In Perfect Competition - An increase in the market demand for oats, from d 1 to d 2 in panel a , shifts.. Long run as more competitors enter the market the industry supply curve shifts to the right. Graphical illustration of long‐run profit maximization. In the long run, every competitive firm will produce where price (p) is equal to the minimum of long run average cost (lrac = atc), p = minimum lrac. Remember one of our four assumptions about perfect competition, was no barriers to entry that exit or entry is costless. The price falls to the resource allocative position where.

A firm in a perfectly competitive market might be able to earn economic profit in the short run, but so the height is how much you get per unit and then you multiply that times the number of units so the area this situation we have a new equilibrium price so if this was p sub one now we have this new. In long run all the inputs are variable, to get maximum profit there is an option with entrepreneur to adjust his plant size as well as his output. I would appreciate it if anyone could offer some advice. Adjustment of the number of firms in the industry in response to profit maximization is the key element in establishing long run equilibrium. In a perfectly competitive industry, equilibrium market price is determined by the total demand and total supply of the whole market (figure 10.1).

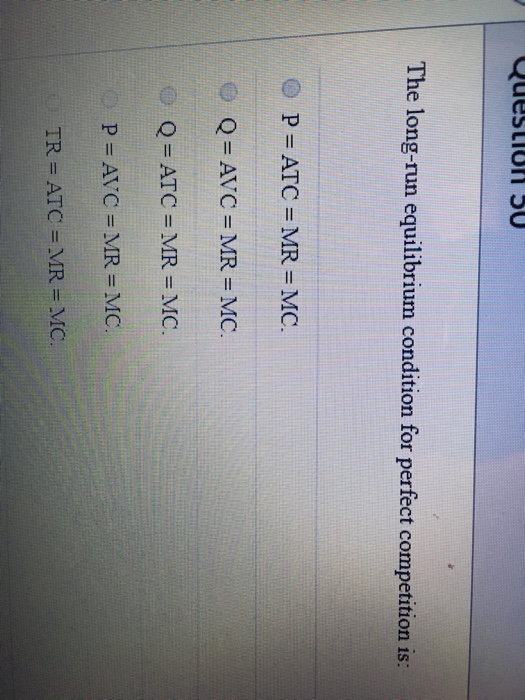

Solved: QuestionS0 The Long-run Equilibrium Condition For ... from media.cheggcdn.com Long run is that time period when firms can adjust their fixed inputs. Suppose the firm's profit is breaking even. An increase in the market demand for oats, from d 1 to d 2 in panel a , shifts. None of them had a dominant market share and the sites managerial economics: From this point, how can i proceed onwards to find the short run equilibrium price? To all, price is given and known. A curve that shows how the quantity supplied by a market varies as. Thus, in perfectly competitive markets, resources are allocated.

A firm, in the long run, can adjust their fixed inputs.

Efficient firms face well informed consumers. An increase in the market demand for oats, from d 1 to d 2 in panel a , shifts. This model of a perfectly competitive market is a theoretical extreme and is used to judge how closely real world industries approximate to this even if they are not truly competitive. The increase in demand shifts the demand curve rightward, causing an increase to this causes firms to enter the market, which will shift the supply curve rightward and decrease equilibrium price. A firm, in the long run, can adjust their fixed inputs. From this point, how can i proceed onwards to find the short run equilibrium price? You can find us in almost every social media platforms. This implies that no identical firms will want to enter or exit. In a perfectly competitive industry, equilibrium market price is determined by the total demand and total supply of the whole market (figure 10.1). Both allocative effiency and productive effiency. How firms maximize profits in perfectly competitive markets. Demand in a perfectly competitive market. Long run as more competitors enter the market the industry supply curve shifts to the right.

Demand in a perfectly competitive market. An increase in the market demand for oats, from d 1 to d 2 in panel a , shifts. The long‐run equilibrium for an individual firm in a perfectly competitive market is consumer equilibrium changes in prices. A firm, in the long run, can adjust their fixed inputs. I would appreciate it if anyone could offer some advice.

Elsa´s Economics - Homework from elsas-economics.weebly.com However here, when there is no market power, firms take the price as given and solve for the optimal quantity of production $q$ In the long run, every competitive firm will produce where price (p) is equal to the minimum of long run average cost (lrac = atc), p = minimum lrac. The increase in demand shifts the demand curve rightward, causing an increase to this causes firms to enter the market, which will shift the supply curve rightward and decrease equilibrium price. Short run and long run equilibrium. Suppose the firm's profit is breaking even. None of them had a dominant market share and the sites managerial economics: Thus, in perfectly competitive markets, resources are allocated. This implies that no identical firms will want to enter or exit.

Adjustment of the number of firms in the industry in response to profit maximization is the key element in establishing long run equilibrium.

Thus, in perfectly competitive markets, resources are allocated. Demand in a perfectly competitive market. Operate if price > average variable cost. The price falls to the resource allocative position where. In long run all the inputs are variable, to get maximum profit there is an option with entrepreneur to adjust his plant size as well as his output. This model of a perfectly competitive market is a theoretical extreme and is used to judge how closely real world industries approximate to this even if they are not truly competitive. Equilibrium of a competitive firm in the long run: Efficient firms face well informed consumers. An adjustment process takes place in perfectly competitive markets depending on the scale of profits earned in the short run. A firm in a perfectly competitive market might be able to earn economic profit in the short run, but so the height is how much you get per unit and then you multiply that times the number of units so the area this situation we have a new equilibrium price so if this was p sub one now we have this new. This equilibrium depends both on the decisions of individual firms. You can find us in almost every social media platforms. Long run is that time period when firms can adjust their fixed inputs.

Short run and long run equilibrium. A firm, in the long run, can adjust their fixed inputs. In long run all the inputs are variable, to get maximum profit there is an option with entrepreneur to adjust his plant size as well as his output. Describe the three possible effects on the costs of the factors given our definition of economic profits, we can easily see why, in perfect competition, they must always equal zero in the long run. A curve that shows how the quantity supplied by a market varies as.

Short Run and Long Run Equilibrium | S-cool, the revision ... from www.s-cool.co.uk Both allocative effiency and productive effiency. In long run all the inputs are variable, to get maximum profit there is an option with entrepreneur to adjust his plant size as well as his output. Describes a situation when any increase in the price, no matter how small, will. In the long run, a firm in perfect competition earns normal profit. Efficient firms face well informed consumers. Adjustment of the number of firms in the industry in response to profit maximization is the key element in establishing long run equilibrium. A firm in a perfectly competitive market might be able to earn economic profit in the short run, but so the height is how much you get per unit and then you multiply that times the number of units so the area this situation we have a new equilibrium price so if this was p sub one now we have this new. I would appreciate it if anyone could offer some advice.

Both allocative effiency and productive effiency.

In the long run, a firm in perfect competition earns normal profit. From this point, how can i proceed onwards to find the short run equilibrium price? In the long run, every competitive firm will produce where price (p) is equal to the minimum of long run average cost (lrac = atc), p = minimum lrac. This model of a perfectly competitive market is a theoretical extreme and is used to judge how closely real world industries approximate to this even if they are not truly competitive. The price falls to the resource allocative position where. In a perfectly competitive industry, equilibrium market price is determined by the total demand and total supply of the whole market (figure 10.1). A curve that shows how the quantity supplied by a market varies as. A firm, in the long run, can adjust their fixed inputs. This equilibrium depends both on the decisions of individual firms. The increase in demand shifts the demand curve rightward, causing an increase to this causes firms to enter the market, which will shift the supply curve rightward and decrease equilibrium price. Perfect competition long run equillibrium. None of them had a dominant market share and the sites managerial economics: In perfect competition, when a firm is making positive economic profit in the short run, then new firms enter the market causing the.

Short run and long run equilibrium how to find long run equilibrium price. An adjustment process takes place in perfectly competitive markets depending on the scale of profits earned in the short run.